View the ORE Academy YouTube Channel

View the ORE Academy YouTube Channel

ORE Academy

Find Out More

Pricing and Risk Modeling Program

Sign up to Hear about the Latest ORE Developments

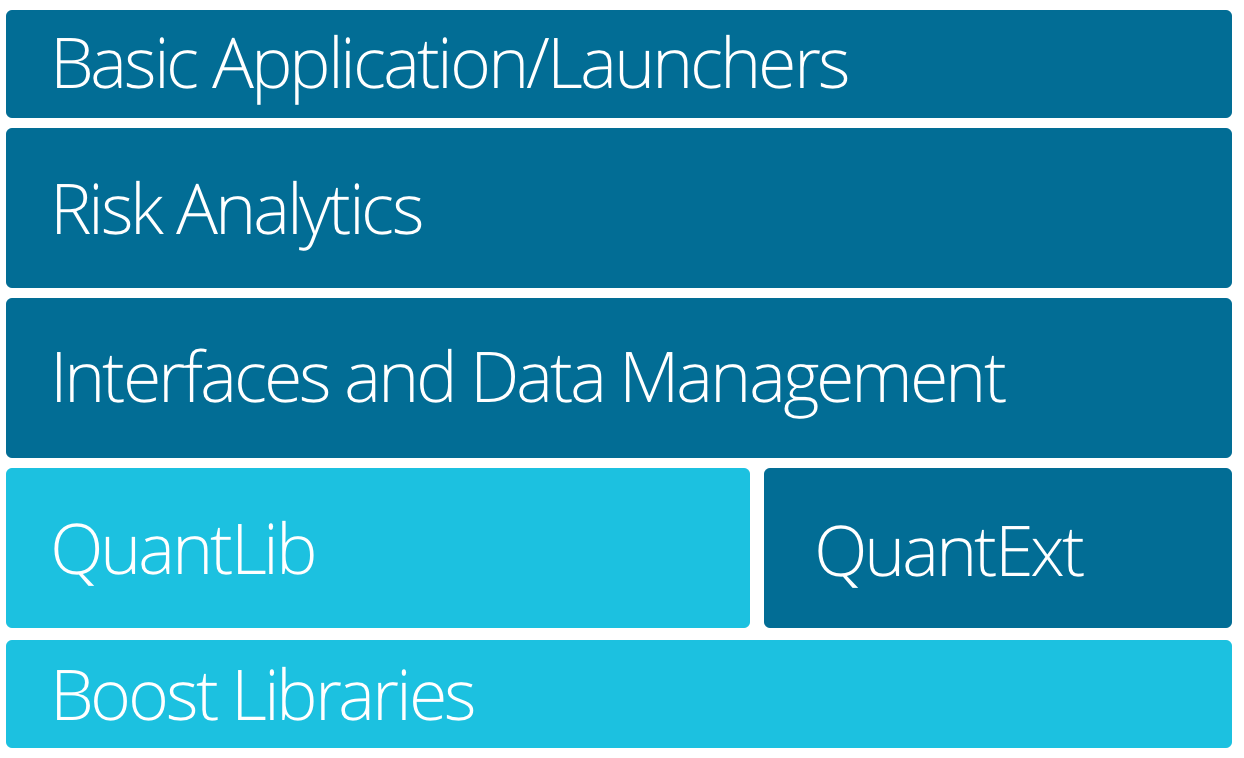

The Open Source Risk Engine’s objective is to provide a free/open source platform for risk analytics and XVA. It is based on QuantLib and grew from work developed by market professionals and academics.

The Open Source Risk project aims at establishing a transparent peer-reviewed framework for pricing and risk analysis that can serve as

- a benchmarking, validation, training, teaching reference

- an extensible foundation for tailored risk solutions

Open Source Risk Engine (ORE) provides

- contemporary risk analytics and value adjustments (XVAs)

- interfaces for trade/market data and system configuration (API and XML)

- simple application launchers in Excel, LibreOffice, Python, Jupyter

- various examples that demonstrate typical use cases

- comprehensive test suites

ORE is based on QuantLib, the open source library for quantitative finance, and it extends QuantLib in terms of simulation models, financial instruments and pricing engines.

ORE is sponsored by Acadia as part of the firm’s commitment to transparency in pricing methods and risk analytics applied in the industry. ORE is free/open software, provided under the Modified BSD License, which permits using and modifying the code base as well as incorporating it into commercial applications.

Open Source Risk Engine is sponsored by Acadia. The concept of open source is integral to the Firm’s vision. ORE is offered to the community as part of that vision and commitment to improve the transparency of risk analytics.

Release Timeline